ACH payments give accounting firms a reliable, low-cost way to collect client payments without the hassle of paper checks or high credit card fees. This guide covers how ACH works, when it makes sense for your firm, and the step-by-step process for setting up electronic payments that run on autopilot.

What are ACH payments?

ACH payments are electronic transfers that move money directly between bank accounts through the Automated Clearing House network. This network, governed by the National Automated Clearing House Association (NACHA), provides a secure and low-cost way for accounting firms to collect client payments without relying on paper checks, which now represent just 26% of B2B payments or expensive wire transfers.

The ACH network processes transactions in batches throughout each business day. Funds typically settle within one to three business days, though same-day options exist when you need faster processing. This timeline makes ACH particularly well-suited for recurring billing situations like monthly retainers or subscription-based advisory services., with Same Day ACH volume increasing 45% in 2024. This timeline makes ACH particularly well-suited for recurring billing situations like monthly retainers or subscription-based advisory services.

There are two types of ACH transactions your firm should understand:

- ACH debits: Your firm pulls funds directly from a client’s bank account after they authorize the transaction

- ACH credits: Clients push funds from their bank account to yours, similar to paying a bill online

For accounting firms, ACH solves a fundamental problem. You get paid consistently without chasing invoices or processing paper checks. Clients increasingly expect modern payment options, and ACH delivers that while cutting down on your administrative work., which 63% of organizations faced fraud issues with in 2024. Clients increasingly expect modern payment options, and ACH delivers that while cutting down on your administrative work.

Should your accounting firm accept ACH payments?

ACH works best for accounting firms with predictable, recurring billing relationships. If you invoice clients monthly, offer retainer arrangements, or provide subscription-based services, ACH can transform how cash flows into your firm.

Consider accepting ACH payments if your firm:

- Processes multiple client invoices each month

- Offers retainer or subscription-based advisory services

- Spends significant time following up on unpaid invoices

- Wants to reduce the administrative burden of check processing

- Serves clients who prefer electronic payments over credit cards

ACH may be less critical if your firm primarily handles one-time engagements with immediate payment requirements. However, even project-based firms benefit from offering ACH as an option for clients who prefer it. The setup cost is minimal, and having the capability ready means you won’t scramble when a client asks for it.

How to accept ACH payments at your firm

Setting up ACH payments involves four key steps. You’ll select a payment platform, establish your merchant account, collect client authorization, and then process transactions. Each step builds on the previous one to create a streamlined payment workflow that runs with minimal ongoing effort.

Step 1: Choose a payment platform built for accounting firms

Your payment platform should integrate with your existing accounting software and simplify the client experience. Generic payment processors often lack the features accounting firms need for efficient reconciliation and client management. You’ll spend more time working around the system than benefiting from it.

When evaluating platforms, prioritize these capabilities:

- Accounting software integration: Direct sync with QuickBooks, Xero, or your current system eliminates manual data entry

- Client payment portal: Allows clients to authorize payments and view invoices without friction

- Automated reconciliation: Payments match to invoices automatically, saving your team hours each month

- NACHA compliance: Ensures your firm meets security standards for handling banking information

The right platform feels like an extension of your existing workflow rather than another system to manage. Look for solutions designed specifically for professional services firms rather than retail or e-commerce businesses.

Step 2: Set up your ACH merchant account

A merchant account connects your firm to the ACH network and allows you to process electronic payments. Think of it as the bridge between your payment platform and the banking system. You’ll need an active business bank account and approval from your payment processor to get started.

The setup process typically requires your business bank account information, federal tax ID, business license, and basic company details including ownership information. Most processors approve applications within one to three business days, so you won’t wait long to start accepting payments.

You don’t need a separate bank account for ACH. Your payment processor deposits funds directly into your existing business account alongside your other deposits.

Step 3: Collect client authorization

NACHA regulations require explicit client authorization before you can pull funds from their bank account. This protects both your firm and your clients from unauthorized transactions. Without proper authorization, you can’t initiate ACH debits.

Authorization can happen through online forms, email consent, or recorded phone calls. The authorization should include the client’s name, bank account and routing numbers, permission to debit their account, and instructions for revoking consent.

Most modern payment platforms handle this through a secure digital form that clients complete in minutes. The client enters their banking information directly into the platform, so your team never sees or handles sensitive account numbers. This approach is faster and more secure than collecting information manually.

Step 4: Process and reconcile payments

Once clients authorize ACH payments, you can initiate transactions through your payment platform’s dashboard. For recurring engagements, set up automatic billing to eliminate monthly invoicing tasks entirely. The system pulls funds on your schedule without any manual intervention.

Best practices for ongoing ACH management include:

- Schedule recurring payments: Automate retainer billing to ensure consistent cash flow without monthly effort

- Monitor failed transactions: Watch for insufficient funds or authorization issues and follow up promptly

- Reconcile regularly: Match incoming payments to invoices in your accounting software

- Maintain documentation: Keep authorization records for compliance and audit purposes

The goal is to create a system that runs itself. Once you’ve set up a client on recurring ACH, you shouldn’t need to think about their payments again unless something goes wrong.

What to look for in an ACH payment solution

The right ACH solution reduces administrative work while improving the client payment experience. For accounting firms, this means choosing a platform designed for professional services rather than generic retail transactions. The features that matter to a restaurant or online store aren’t the same ones that matter to your firm.

Essential features to evaluate include batch processing so you can handle multiple client payments simultaneously, detailed reporting for reconciliation and audits, client self-service portals where clients can view invoices and update their own banking information, and responsive support when you need help during busy season.

Avoid platforms that require manual data entry between systems, charge excessive per-transaction fees, or lack clear reconciliation tools. These limitations create more work than they eliminate. You’ll end up spending time fighting the system instead of serving clients.

How much do ACH payments cost?

ACH processing fees are significantly lower ACH processing fees are typically 40% lower than credit card fees. This makes them ideal for accounting firms with high-value invoices or frequent billing cycles. Most processors charge a combination of percentage-based and flat per-transaction fees.

| Payment method | Typical cost | Best for |

| ACH | 0.5–1.5% plus $0.20–$1.50 per transaction | Recurring billing, high-volume invoicing |

| Credit card | 2–3% plus per-transaction fee | One-time, client-initiated payments |

| Wire transfer | $10–$50+ flat fee | Urgent transfers, large amounts |

| Paper check | Administrative time and processing cost | Low-frequency payments |

For a firm billing $50,000 monthly across 20 clients, ACH could save hundreds of dollars compared to credit card processing. Those savings compound over time, especially for firms with retainer-heavy revenue models. The money you save on processing fees goes directly to your bottom line.

Benefits of ACH payments for accounting firms

ACH addresses specific pain points that accounting firms face around cash flow predictability, administrative efficiency, and client convenience. The benefits extend beyond just lower fees.

- Lower transaction costs: Protect your margins on recurring invoices compared to credit card fees

- Predictable cash flow: Automated recurring payments mean consistent income without chasing clients

- Reduced administrative work: Eliminate manual invoice follow-ups and check processing

- Higher payment success rates: Clients rarely change bank accounts, so you see fewer failed payments than with expired credit cards

- Better for high-value invoices: No per-transaction caps or chargeback risks like credit cards

- Compliance-friendly: Clear authorization trails help with audits and documentation requirements

The combination of lower costs and automation creates a compounding effect. You spend less time on collections, experience fewer payment failures, and keep more of what you bill.

Are ACH payments secure?

ACH is one of the most secure payment methods available. It’s regulated by NACHA and federal banking authorities, with multiple layers of protection safeguarding both your firm and your clients’ banking information.

Security measures built into ACH include bank-level encryption that protects data in transit and at rest, account verification through microdeposits or instant verification before processing, tokenization that converts banking information to secure tokens rather than storing plain text, fraud detection that monitors transactions for suspicious patterns, and authorization requirements that ensure clients explicitly consent before funds can be pulled.

Your payment processor handles the technical security requirements. Your responsibility is following proper authorization procedures and maintaining documentation. As long as you collect authorization correctly and work with a reputable processor, ACH is extremely safe.

ACH payments vs. wire transfers

Both ACH and wire transfers move money electronically, but they serve different purposes. Understanding when to use each helps you choose the right tool for each situation.

| Feature | ACH payments | Wire transfers |

| Speed | One to three business days | A few hours to two days |

| Cost | Under $2 per transaction | $10–$50+ per transaction |

| Best for | Recurring billing, multiple payments | Urgent transfers, large amounts |

| Geographic scope | US and Puerto Rico | International |

| Reversibility | Can be disputed if issues arise | Difficult to reverse |

For routine client billing and retainers, ACH is the clear choice due to lower costs and automation capabilities. Reserve wire transfers for urgent situations, international payments, or when clients specifically request them. Most accounting firms find that ACH handles the vast majority of their payment needs.

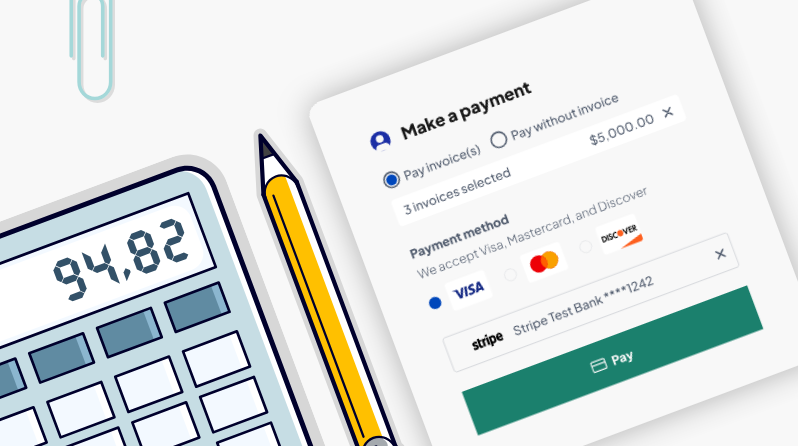

How Aiwyn Payments simplifies ACH payments for accounting firms

Aiwyn Payments is built specifically for accounting firms, handling ACH payments while integrating with your existing software and client workflows. Rather than forcing you to adapt to a generic payment system, Aiwyn Payments fits into how your firm already operates.

What sets Aiwyn Payments apart is native accounting software integration that syncs directly with QuickBooks Online, Xero, and other platforms you use daily. Clients authorize payments through a simple, branded portal with just a few clicks. Payments match to invoices automatically without manual data entry, and you can bill multiple clients simultaneously through batch processing.

The result is less time spent on payment administration and more time for billable work. Your clients get a modern payment experience that reduces friction and improves their perception of your firm. Schedule a demo to see how Aiwyn simplifies ACH payments for your firm.

Frequently asked questions about ACH Payments

ACH payments typically settle within one to three business days, depending on your bank and payment processor. Some providers offer same-day ACH for faster settlement, though this may incur an additional fee.

Yes, clients can dispute ACH payments within a set timeframe if there’s an error or unauthorized charge. Proper authorization documentation protects your firm and makes the dispute process more straightforward than credit card chargebacks.

Your processor will notify you if a payment fails due to insufficient funds or incorrect account details. You can then follow up with the client to correct the issue and retry the payment.

Yes, once a client authorizes ACH, you can schedule recurring payments for retainers, subscriptions, or any predictable billing cycle. This eliminates the need to manually invoice each month.

To learn more about managing ACH payments with Aiwyn Payments, request a personalized demo and learn how our modern solution makes it easy for accounting firms to streamline their billing operations today.